10 Practical Ways to Keep Money Without Constant Financial Stress

Most people do not struggle financially because they earn too little. They struggle because money does not stay with them for long. Income may be regular and expenses may seem reasonable, yet savings fail to build over time. This creates frustration because the effort of earning does not translate into stability. Learning how to keep money is less about increasing income and more about managing what happens after money enters your account.

When income increases without any change in habits, spending usually increases as well. This is why people at very different income levels often experience similar financial pressure. Without basic systems in place, money is absorbed by everyday expenses, convenience spending, and gradual lifestyle changes. Addressing this issue does not require extreme discipline. It requires consistency and a clearer understanding of how money is used.

1. Pay Yourself First

Saving whatever remains at the end of the month is unreliable because expenses tend to expand. Paying yourself first changes the order. A fixed portion of income is moved to savings as soon as it is received.

Over time, this becomes easier to maintain because spending adjusts naturally to the remaining balance. Saving stops feeling optional and becomes part of the routine, which makes it one of the more dependable ways to keep money over long periods.

2. Understand Spending Patterns, Not Just Totals

Knowing the total amount spent each month does not explain where money actually goes. Many expenses happen out of habit or convenience rather than deliberate choice.

Tracking spending over time reveals patterns that are otherwise easy to miss. Once these patterns are clear, changes can be made more thoughtfully. This approach reduces unnecessary spending without forcing rigid rules.

3. Keep Money Aside by Building an Emergency Fund

Unexpected expenses are a normal part of life. Without an emergency fund, these expenses often lead to debt or force people to use long-term savings. An emergency fund helps absorb these disruptions. Even a partially built fund reduces financial pressure and prevents setbacks that undo months of progress. This makes it easier to keep money allocated to its intended purpose. Even starting with a small amount like one month’s expenses can provide a safety net and reduce financial stress immediately.

4. Automate Savings Wherever Possible

Saving manually depends on motivation, which varies. Automation removes the need to make repeated decisions. When savings are automated, consistency improves. Over time, money accumulates steadily without requiring constant attention, which supports financial stability. Even small, regular investments can grow significantly over time thanks to compounding, helping you keep money for bigger goals.

5. Reduce Low-Value Spending

Some expenses contribute meaningfully to daily life, while others continue simply because they have become routine. Reducing spending that offers little real value is more effective than cutting everything evenly. This allows money to be redirected without significantly affecting quality of life. The result is a financial structure that feels manageable rather than restrictive.

6. Limit Exposure to High-Interest Debt

High-interest debt increases financial strain over time. While borrowing may sometimes be necessary, interest payments reduce future flexibility. Lowering dependence on high-interest debt allows more income to be used for savings and investments. This improves long-term financial efficiency.

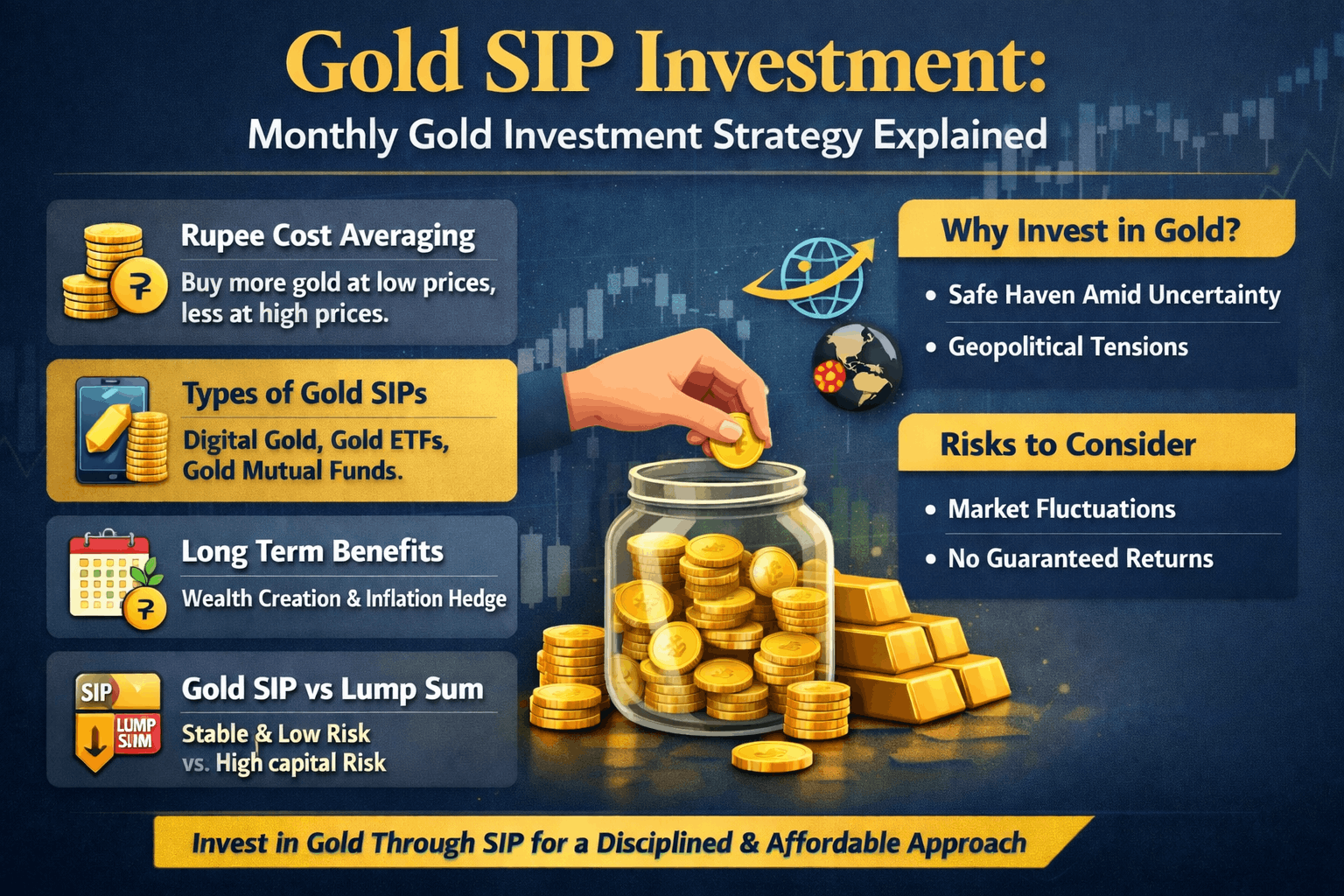

7. Keep Money by Using Appropriate Saving Instruments

Keeping large amounts of cash in low-interest accounts can reduce purchasing power over time due to inflation. While safety is important, ignoring growth entirely has consequences.

Some people choose to diversify savings using different instruments, including gold. Platforms like Dive Money, which now focuses on gold investing, allow individuals to invest gradually through gold SIPs, with mutual fund SIPs planned for launch soon. These options aim to help savings grow rather than remain idle, with potential returns of up to 16% per annum, depending on market conditions.

8. Begin Investing with a Long-Term Perspective

Delaying investment due to uncertainty often leads to missed opportunities. Starting early with small amounts allows time to work in your favour. A long-term approach reduces the impact of short-term market movements and supports steady accumulation through regular contributions.

9. Treat Additional Income as a Strategic Tool

Extra income does not automatically improve financial health. Without a plan, it often leads to higher spending. Allocating a portion of additional income toward savings or investments ensures that extra earnings contribute to long-term improvement rather than short-term consumption.

10. Keep Money by Developing Financial Literacy

Many financial mistakes occur due to lack of understanding rather than carelessness. Basic financial knowledge improves decision-making and reduces uncertainty. Accessing reliable information and building familiarity with financial concepts helps people make consistent choices and avoid common errors.

Why Retaining Money Is Often More Difficult Than Earning It

Earning money usually follows a fixed structure. Retaining it depends on repeated daily decisions. Without systems, small expenses accumulate and gradually weaken financial progress. Keeping money requires patience and regular effort. The results may not be immediate, but over time they lead to greater stability and control.

Frequently Asked Questions

Why do people struggle to keep money despite stable income?

Because spending tends to increase unless it is deliberately managed.

Is it possible to keep money with irregular income?

Yes. Emergency funds and automated saving help manage variability.

Should saving come before investing?

Saving provides security, while investing supports growth. Both serve different purposes.

How long does it take to see financial improvement?

Stress often reduces within a few months, while measurable financial progress takes longer.

What is the most common financial mistake?

Assuming that higher income alone will solve financial problems.