8 Best Investment Options in India to Build Long-Term Wealth

We Indians have always been careful with money. From mothers saving cash in kitchen dabbas to fathers buying land as investment whenever possible, the goal was never luxury. It was security. A future where money problems don’t control life.

But times have changed.

Today, simply keeping money in a savings account is not enough. Prices keep rising, while bank interest struggles to keep up. What feels like saving is often just money slowly losing its value. This is why investing is no longer something only “finance people” do. It has become a basic life skill.

If you are a student, a young professional, or someone trying to make better financial decisions, here are eight investment options in India that actually make sense today, explained in a simple and practical way.

1. Equity Markets and Direct Stocks

Investing in equities means buying ownership in a company. When you purchase a stock, you become a shareholder and benefit if the business grows over time.

India’s stock market offers long-term wealth creation, especially through sectors like technology, renewable energy, manufacturing, and infrastructure. However, stock prices move daily based on earnings, news, and global events. This makes equities volatile in the short term.

Direct stock investing works best for people who can stay invested for several years and are willing to tolerate ups and downs. Young investors have an advantage here because time allows them to recover from market corrections and benefit from compounding.

2. Mutual Funds Investment (Equity and Debt)

Mutual funds invest your money across multiple companies or debt instruments, reducing the risk of depending on a single investment. Equity mutual funds aim for growth, while debt mutual funds focus on stability and predictable returns.

Through SIPs, investors can start with small amounts and invest regularly. This approach helps build discipline and avoids the pressure of timing the market.

Mutual funds are one of the most popular investment options in India for beginners because they offer diversification, professional management, and flexibility.

3. Index Funds and ETFs

Index funds and Exchange Traded Funds invest in companies that make up major indices like the Nifty 50 or Sensex. Instead of selecting individual stocks, these funds reflect the performance of the overall market.

Because index funds follow a fixed structure, they usually have lower costs and less frequent trading. ETFs offer similar exposure but can be bought and sold on stock exchanges like shares.

These instruments are suitable for long-term investors who want steady participation in India’s economic growth without the complexity of stock selection.

4. Fixed Deposits

Fixed Deposits offer guaranteed returns over a fixed period. Bank FDs are insured and considered safe, while corporate FDs provide higher returns but require careful selection.

FDs are best suited for emergency funds and short-term goals. While they offer security and liquidity, their returns often struggle to beat inflation, making them unsuitable as the main tool for wealth creation.

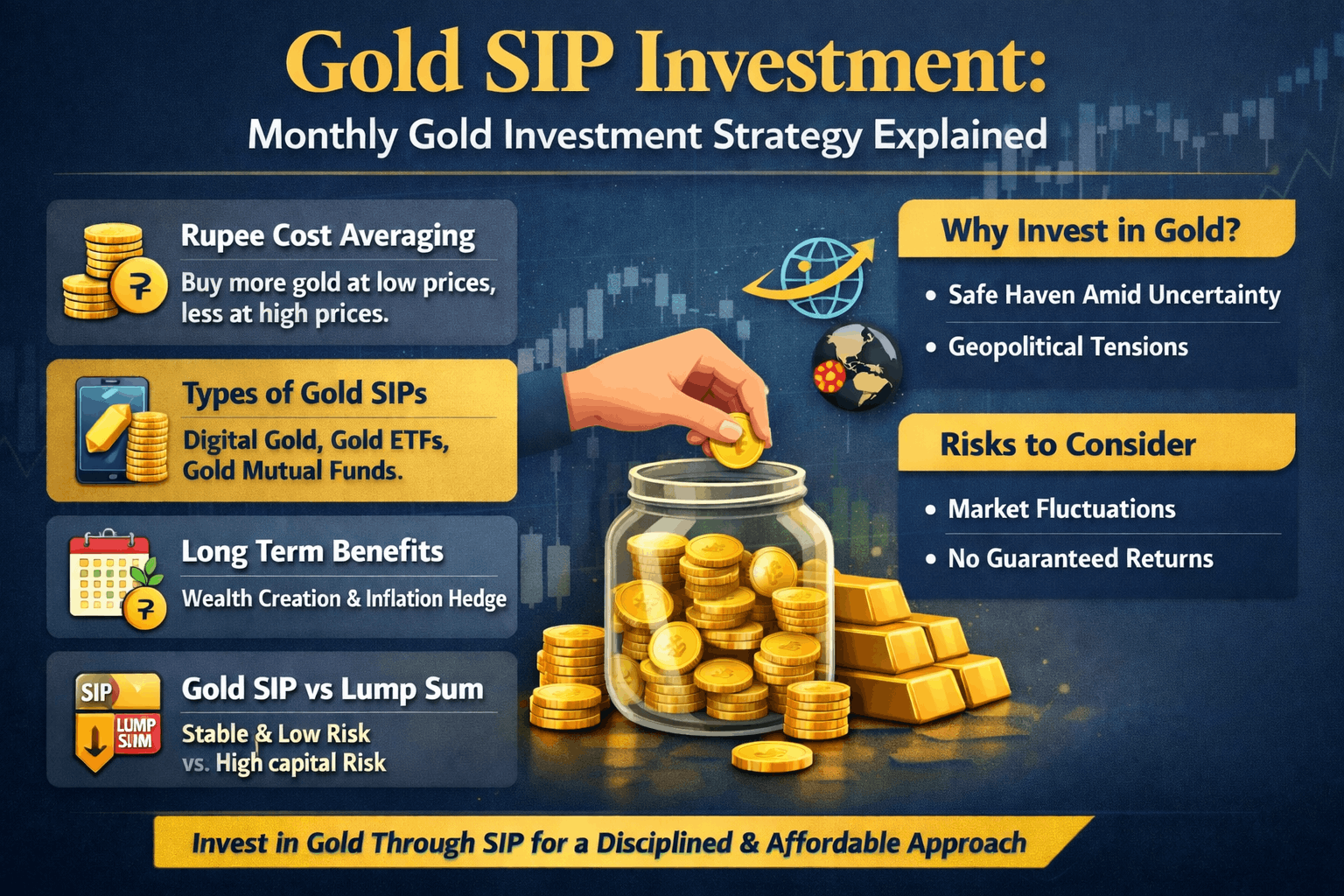

5. Gold Investment (Digital Gold, ETFs and SGBs)

Gold has always been an important part of Indian savings. It acts as a hedge against inflation and performs well during economic uncertainty.

Today, investors can choose from digital gold, gold ETFs, and Sovereign Gold Bonds. Digital gold allows small and flexible investments without worrying about storage or purity.

Platforms like Dive make gold investing accessible by allowing users to start with just ₹100. This makes it easier for students and young earners to build a safety cushion gradually rather than waiting for a large lump sum.

Common perception was that gold adds stability to a portfolio but in recent years gold has outperformed even direct equity investments.

6. Public Provident Fund (PPF)

PPF is a government-backed savings scheme with a 15-year tenure. Contributions qualify for tax deductions, and both interest and maturity amounts are tax-free.

Although the money is locked in for the long term, partial withdrawals are allowed after a few years. PPF is ideal for retirement planning and for investors who prefer guaranteed returns with minimal risk.

7. Bonds (Corporate and Government)

Bonds are fixed-income instruments where investors lend money to companies or the government in exchange for regular interest payments.

Corporate bonds usually offer higher returns than government bonds but come with higher risk depending on the issuer’s credit rating. Bonds provide predictable income and help reduce overall portfolio volatility.

They are useful for investors who want stability without completely avoiding returns.

8. Real Estate Investment

Real estate has long been considered a reliable investment in India. Property can generate returns through rental income as well as long-term price appreciation.

However, real estate requires large upfront capital, involves maintenance costs, and is less liquid compared to financial investments. It works best as a long-term investment for people with stable income and surplus funds.

For young investors, real estate exposure can also come indirectly through Real Estate Investment Trusts (REITs), which require lower investment amounts and offer regular income.

Final Thoughts

Investing is not about starting big or finding perfect opportunities. It is about understanding where your money goes and staying consistent over time. India’s economy is growing, and those who start early have a clear advantage. Begin with what you can afford, keep learning, and allow time to do the heavy lifting.